Commission calculation in Indian insurance looks simple on paper — premium × commission percentage = your earning. In practice, it's anything but. A working agent handles four to twelve insurers at any time, each with their own product-specific slab tables, each with different renewal commission rules, each with their own TDS treatment. Add in two or three sub-agents below you and the math becomes a daily exercise in error-checking. This guide breaks down how commission is actually calculated in Indian insurance — first-year, renewal, multi-insurer, sub-agent splits, TDS — and what a real insurance commission calculator app needs to handle for you.

For Indian agents specifically, the calculation gets more complex because of how different lines of business are structured. Life insurance pays heavy first-year commission (FYC) with thinning renewals. Motor insurance pays lower FYC but more consistent renewals. Health insurance falls somewhere in the middle. Mix all three in your book and you've got a multi-line commission picture that no single spreadsheet can hold cleanly for long. This is exactly why a proper commission reconciliation software matters once your book grows beyond a few hundred policies.

FYC vs Renewal Slabs — Understand The Curve

The single biggest concept in commission economics is the difference between First-Year Commission (FYC) and Renewal Commission. FYC is the front-loaded incentive that motivates agents to sell new policies — it's typically much higher per rupee of premium than renewal commission, but it only happens once per policy.

Approximate ranges for Indian agents (these vary by insurer, product and time period, so always verify with your insurer's current circular):

- Life Insurance (LIC, term, endowment): FYC typically 25-40% of first-year premium, renewals drop to 5-10% from year 2 onwards.

- Health Insurance: FYC around 15-25% of premium, renewals 12-18%. Lower FYC drop, more sustainable income stream.

- Motor (OD component): Typically 10-15% on Own Damage portion. Third-party premium has regulated lower commission.

- General Insurance (Home, Shop, Fire): 10-15% with relatively flat renewal commission.

The implication for an agent's earning strategy is clear: life insurance gives you a big upfront commission but lower long-term recurring income; health and general insurance build more steady recurring streams. A diversified book balances both. An insurance commission calculator app that handles all of these in one view lets you make this strategic mix decision with actual data instead of intuition.

Multi-Insurer Variations — Why Manual Tracking Fails

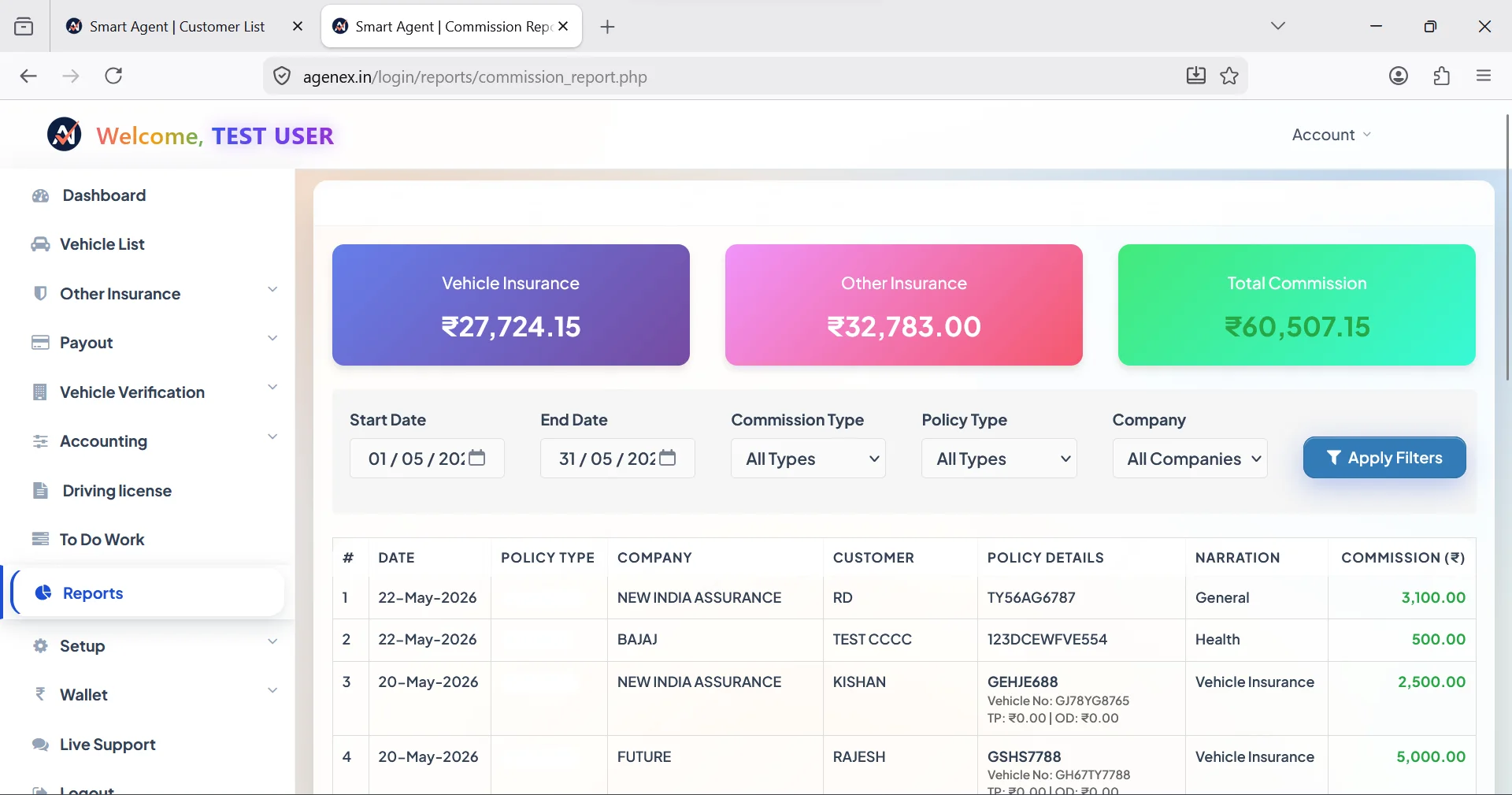

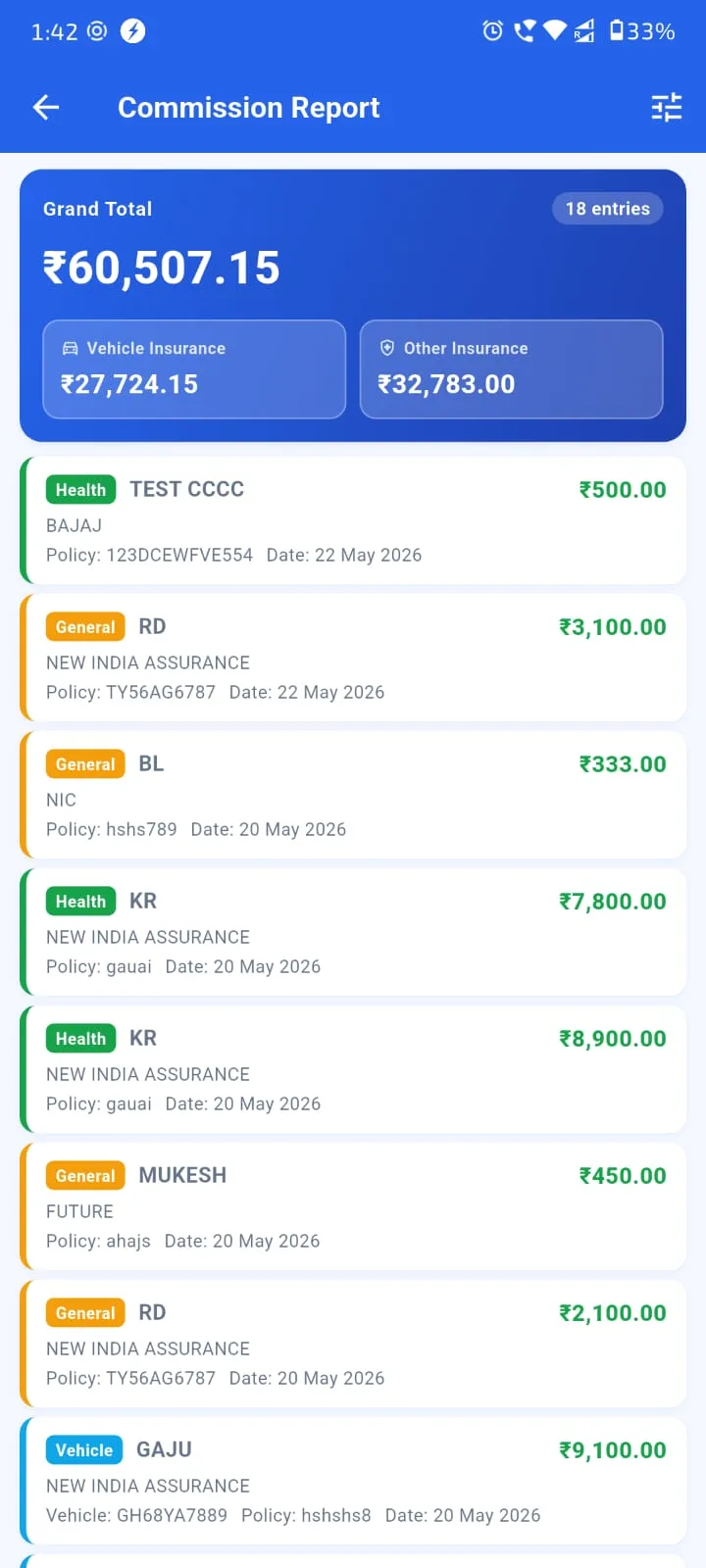

Each insurer in India publishes its own commission circular with its own product-specific slabs. LIC alone has dozens of product variants with their own commission tables. Health insurers — Star, HDFC ERGO, Niva Bupa, Care, Manipal Cigna, Reliance General, ICICI Lombard, Bajaj Allianz, TATA AIG — each have their own slab structures. Motor insurers similarly.

Maintaining all this manually in Excel is practically impossible for a multi-carrier broker. The slabs change periodically. New products get added. Existing slabs get revised by insurers without much notice. A working multi carrier quoting software with a properly maintained commission slab database becomes essential — you focus on selling, the software handles the commission math.

The practical impact: when you're sitting with a client and offering three insurer options for the same coverage need, your insurance digital assistant app shows you the commission you'd earn from each option. You can have an honest conversation with the client about coverage quality while also knowing which option keeps your agency healthy. This is the kind of transparent, data-informed selling that builds long-term agent reputations.

Try Agenex Free

Every Agenex feature is included on a free trial — no credit card required. The insurance commission calculator app with multi-insurer slab database is built in.

Start Free TrialSub-Agent Split Math — Where Most Disputes Start

If you have POSPs or sub-agents working under you, every commission calculation has another layer — the split between you and the sub-agent. Common arrangements in India: 70/30 (sub-agent keeps 70%, you keep 30%), 60/40, 50/50, or product-specific splits where motor lines have one split and health lines have another.

The math gets tricky because the split sits between the insurer's gross commission payment and the TDS deduction. Different agencies handle this differently — some apply TDS on the gross before split, some on the net after split, some pass through TDS proportionally. Whatever your specific arrangement, the calculation needs to be consistent, transparent, and immediately visible to both you and the sub-agent.

This is where a proper commission reconciliation software with built-in split logic earns its keep. Every commission line in your ledger shows: gross from insurer, sub-agent share with their custom %, your retained share, TDS treatment, and current settlement status. Each sub-agent sees their own ledger with the same transparency. Disputes drop to near-zero because there's a single source of truth that both parties trust. PoSP agent registration app users especially benefit because their sub-network growth depends on clean settlement experiences.

TDS and Final Take-Home

TDS (Tax Deducted at Source) is the final layer. Indian insurers deduct TDS on commission payments above a threshold under Section 194D for life and Section 194H for general. The typical rate is around 5%, though this can change with tax circulars — always check current rates with your CA.

Your effective take-home looks like this: Gross commission from insurer → minus sub-agent share (if applicable) → minus TDS deducted at source → equals net take-home. At year-end, your CA claims TDS credit against your income tax liability — so the TDS isn't lost, just timing-shifted. But if your records don't track TDS cleanly per policy per insurer, you'll struggle at filing time and may miss legitimate refunds.

A proper client portfolio manage karne wala app captures TDS on every commission entry, builds a per-insurer TDS summary you can match against Form 26AS at year-end, and exports a clean record for your CA. This is the difference between filing accurate tax returns and paying more tax than you should.

Practical Calculation Walkthrough

Let's walk through one motor policy as a concrete example. A new motor OD policy with ₹15,000 own-damage premium and ₹6,000 third-party premium. Insurer's commission rate: 12% on OD, 2.5% on TP. Sub-agent arrangement: 70/30 split. TDS rate: 5% on gross commission.

- OD commission: ₹15,000 × 12% = ₹1,800

- TP commission: ₹6,000 × 2.5% = ₹150

- Gross commission: ₹1,950

- Sub-agent share (70%): ₹1,365

- Your retained share before TDS: ₹585

- TDS on your share (if cumulative crosses threshold): 5% = ₹29.25

- Your net take-home: ₹555.75

Now multiply this kind of calculation across 100 policies a month with varying insurers, products, premiums, sub-agent arrangements and TDS thresholds. The complexity compounds quickly. A working insurance agent app with built-in commission engine handles every one of these calculations automatically the moment the policy is saved. You see net earnings clearly. Sub-agents see their share clearly. End-of-month statement matches everyone's expectations. Insurance lead manage kaise kare ka practical part is also this — clean money trails build trust both with sub-agents and with your own books.

FAQ

Life insurance — typically 25-40% in year 1 depending on insurer and product. Endowment, term and ULIP all sit in this range but with different renewal commission profiles.

For life insurance, sharply — to 5-10% in year 2 and similar thereafter. For health and motor, the drop is more gradual since FYC is lower to begin with. Diversify your book to balance these patterns.

Typically after insurer pays gross commission, before TDS netting. Specific timing depends on your agency arrangement — a good commission reconciliation software lets you configure this per sub-agent.

Around 5% above the threshold under Section 194D (life) and 194H (general). The exact rate and threshold can change with tax circulars — confirm with your CA for the current financial year.

Yes — Agenex's commission engine maintains slab tables across LIC, Bajaj, ICICI Lombard, HDFC ERGO, Reliance, Star Health, Niva Bupa, Care, TATA AIG, New India and 30+ other insurers. The right commission gets applied automatically per policy entry.

Yes — configure each sub-agent's split percentage once, and every policy they generate is automatically split, with TDS treatment applied correctly. End-of-month statement PDFs are generated per sub-agent and per insurer.

Yes — full functionality in the free Android insurance agent app. You can run a commission scenario sitting in a client meeting, on your phone, without opening a laptop.