A working commission calculator for an insurance agent isn't just a math tool. It's a daily decision-making instrument that quietly shapes which products an agent pushes, which insurer they recommend, and how they pitch a policy to a hesitant client. The best insurance commission calculator app does double duty — estimates earnings before the sale to help with quote conversations, and tracks actual accrued earnings after the sale to keep the agency's commission MIS honest. This guide explains both uses, common mistakes Indian agents make with commission calculations, and what a modern commission reconciliation software setup looks like in 2026.

If you sell across multiple insurers, your commission slabs differ for every product. LIC term, LIC endowment, LIC ULIP — each has different first-year and renewal commission percentages. Same product across Bajaj, ICICI, HDFC ERGO and Reliance can pay very different commissions. Without a structured calculator, agents default to "what feels right" — which usually means recommending the products they remember best, not the ones that actually earn most. A real calculator inside your insurance agent app changes that pattern.

Pre-Sale Estimator — Quote Confidence

The pre-sale use case is the most under-appreciated. Picture a typical sales call: client asks about a term plan + ULIP combination. You quote premiums from three insurers. The client asks "which one is best for me?" You give an honest recommendation based on coverage and reputation. But silently you're also wondering "which one earns me more for the same effort?" That's not a bad question — it's the question every agent has to answer to stay profitable.

A pre-sale estimator inside your insurance digital assistant app shows you, in real time, the projected first-year commission and renewal commission for each option you're quoting. You can structure your recommendation honestly while also knowing which path keeps your business viable. Plug in product, insurer, premium amount and policy tenure. The calculator returns expected first-year commission (FYC) and the projected renewal commission stream. No mental math during a client call. No "let me check and get back to you" delays.

Post-Sale Tracking — Reality Check

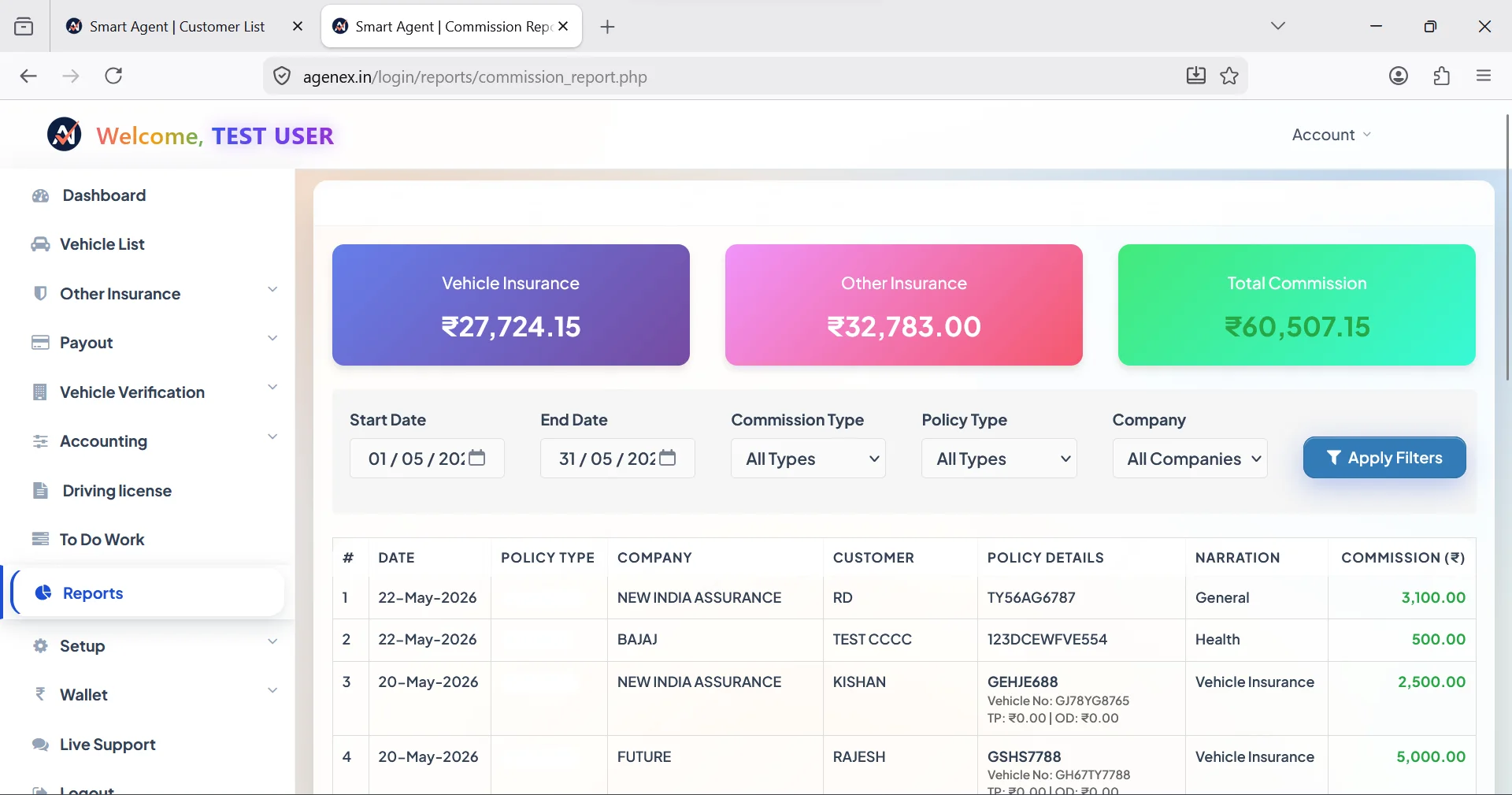

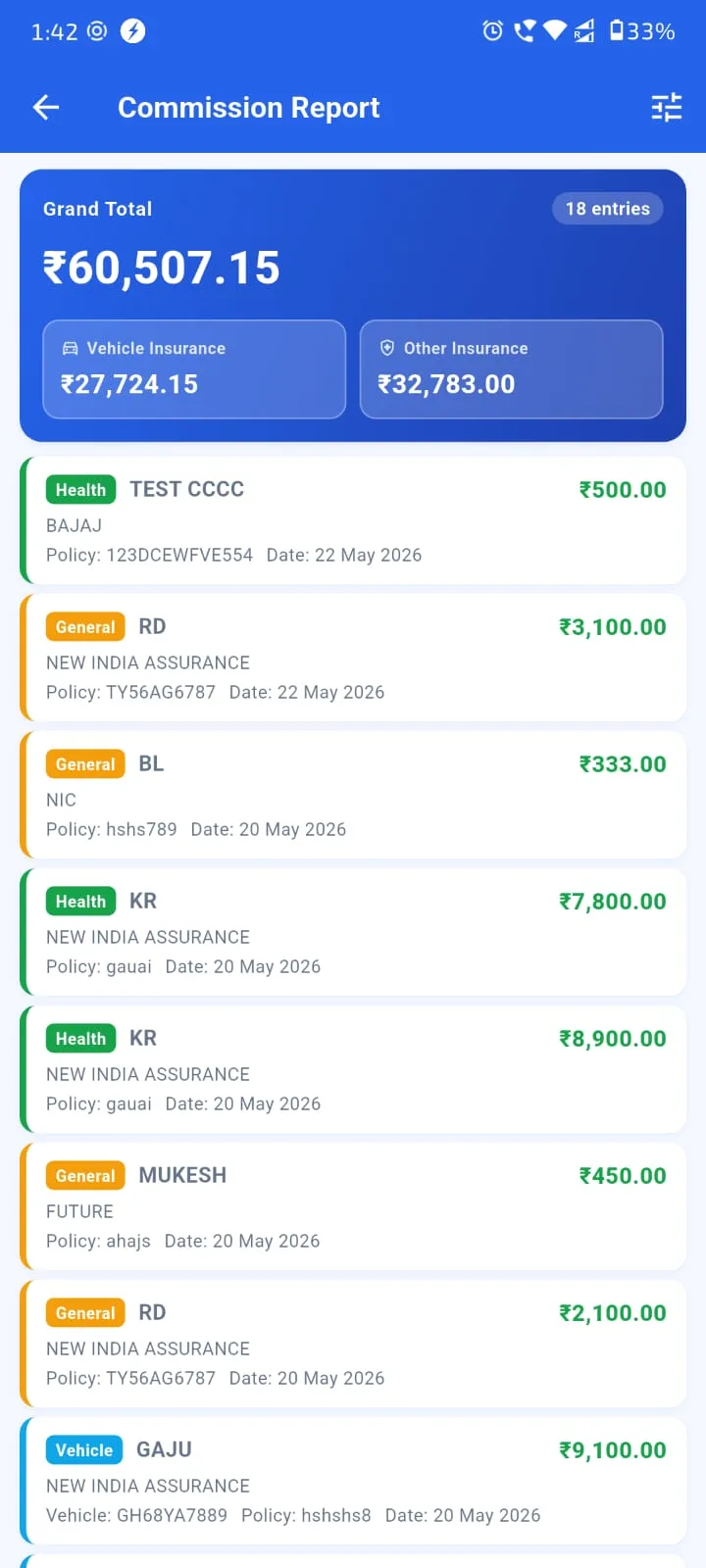

Estimating is one thing. Tracking is another. Once a policy is sold, the calculator transitions into a tracker. The estimated commission becomes an expected accrual. Then when the insurer pays out — usually with TDS deducted, sometimes with claw-back adjustments — the actual earnings are recorded against the same record. The difference between estimated and actual is exactly the gap that commission reconciliation software exists to close.

Over time, this tracker also builds your historical earning data: which insurer pays cleanest, which has the longest payout cycle, which most often disputes commissions, which deducts highest TDS. This is the data that helps a multi-carrier broker prioritize their relationships. A multi carrier quoting software with built-in commission tracking effectively becomes your "which insurer should I sell more of" advisor.

Try Agenex Free

Every Agenex feature is included on a free trial — no credit card required. The insurance commission calculator app for Indian agents is built right in.

Start Free TrialMulti-Insurer Comparison — The Honest Recommendation Path

The real magic of a working commission calculator is multi-insurer comparison. Same client profile, same coverage need — but you can quickly model three or four insurer options side by side. Premium, sum insured, coverage scope, your commission on each one. This isn't about chasing the highest commission at all costs — it's about making informed recommendations where you balance client benefit and agency viability.

For health insurance specifically, this comparison matters because individual-vs-floater, with-or-without riders, single-vs-multi-year tenures, all change both client value and your commission. A 35-year-old asking for a ₹10-lakh family floater gives very different commission outcomes across Star, HDFC ERGO, Niva Bupa, Care, Manipal Cigna and Reliance General. A calculator that shows you all six at once, in the same view, is what separates an old-school agent making decisions on instinct from a modern best insurance CRM for agents user making decisions on data.

Annual Income Forecasting — Plan Your Year

Aggregate calculator data across all your active policies and you get something most agents have never seen: a real annual income forecast. Recurring renewal commission from each existing policy + first-year commission from new business at current run rate = projected total earnings for the year.

This number changes everything. You can see, by month, what your minimum guaranteed income looks like from renewals alone. You can see how much of your annual target you've already secured. You can plan personal expenses, family commitments, agency hiring, sub-agent additions — all with real numbers, not optimistic guesses. Insurance lead manage kaise kare ka deeper question is "where should my time go this month" — and only a real income forecast can answer it.

Common Mistakes Indian Agents Make

A few patterns we see repeatedly across LIC agents, POSPs and motor brokers in India:

Mistake 1 — Ignoring renewal commission: Most agents focus on first-year commission (FYC) and forget that renewal commission, while smaller per policy, compounds over time. A clean health insurance book that renews steadily becomes a passive income stream — but only if you actually track it. Without a calculator, agents tend to undervalue this and over-prioritize new business.

Mistake 2 — Not accounting for TDS: Insurers deduct TDS on commission payments above threshold. Your displayed "earned commission" is gross; what hits your bank is net. A proper commission reconciliation software shows both — and at year-end, your CA can claim TDS credit against income tax. Without it, you either over-estimate your earnings or under-claim TDS at filing time.

Mistake 3 — Treating commission slabs as fixed: Many insurers adjust their commission structures annually, especially for general insurance. If your calculator is built on outdated slab data, your forecasts will be systematically wrong. A client portfolio manage karne wala app with regularly updated insurer commission tables protects you from this.

Mistake 4 — Forgetting sub-agent splits in the math: If you have POSPs or sub-agents working under you, every commission accrual needs to factor their share. Doing this manually at month-end is where most agency disputes happen. PoSP agent registration app users particularly benefit when sub-agent split logic is baked into the calculator itself — disputes drop to near-zero.

FAQ

Yes — both. The same calculator estimates expected commission during the quote stage, then tracks actual accruals after the policy is issued. The difference between estimated and actual becomes the basis of monthly reconciliation.

Yes. For the same coverage requirement, you can run side-by-side commission calculations across multiple insurers and products — useful for honest multi-carrier recommendation conversations.

Yes. Aggregating renewal commission from existing policies plus projected first-year commission from new business at your current pace gives you a working annual income forecast. Useful for personal financial planning and agency target-setting.

Yes — included in every Agenex plan from Silver (Rs.999/year) onwards. There's no separate calculator product to buy.

Yes — full feature parity in the free Android insurance agent app. You can run a commission comparison sitting in a client meeting, on your phone, without opening a laptop.

Yes — LIC endowment, term, money-back, ULIP and other product-specific commission structures are pre-loaded. This is one of the reasons Agenex is widely used as the best app for LIC agents.

Yes — if a policy is being booked under a sub-agent's code, the calculator automatically shows the split between sub-agent share and your retained share. Useful for transparency and avoiding month-end disputes.