Insurance commission income in India is taxed at multiple points — TDS at source, income tax at filing, and GST in certain cases. Most agents handle this poorly because they rely on their CA only at year-end, by which time it's too late to optimize. The agents who keep more of their commission do three things consistently: track every deduction through the year, maintain clean records that match Form 26AS, and understand which expenses they can legitimately claim. This guide walks through how Indian insurance agent commission is actually taxed, what to track monthly, and how a proper commission reconciliation software setup makes year-end filing painless. Always verify current rates and thresholds with your CA before filing — tax rules change year to year. Related: Commission Tracking Software and Calculate Insurance Commission.

TDS On Insurance Commission

Insurers deduct TDS at source on commission paid to agents. The current rate for individual agents is typically 5% under Section 194D for life insurance commission and Section 194H for general insurance commission. There's a threshold below which TDS doesn't apply (typically Rs.15,000 in a financial year per insurer). Above that, every commission payment is subject to TDS deduction.

The practical implication: what hits your bank account is net of TDS. Your gross commission earned is higher than what you've received. At year-end, your CA claims TDS credit against your income tax liability — the TDS isn't lost, just timing-shifted. But if you don't track TDS cleanly per insurer per policy, you'll either over-claim (triggering scrutiny) or under-claim (paying more tax than necessary).

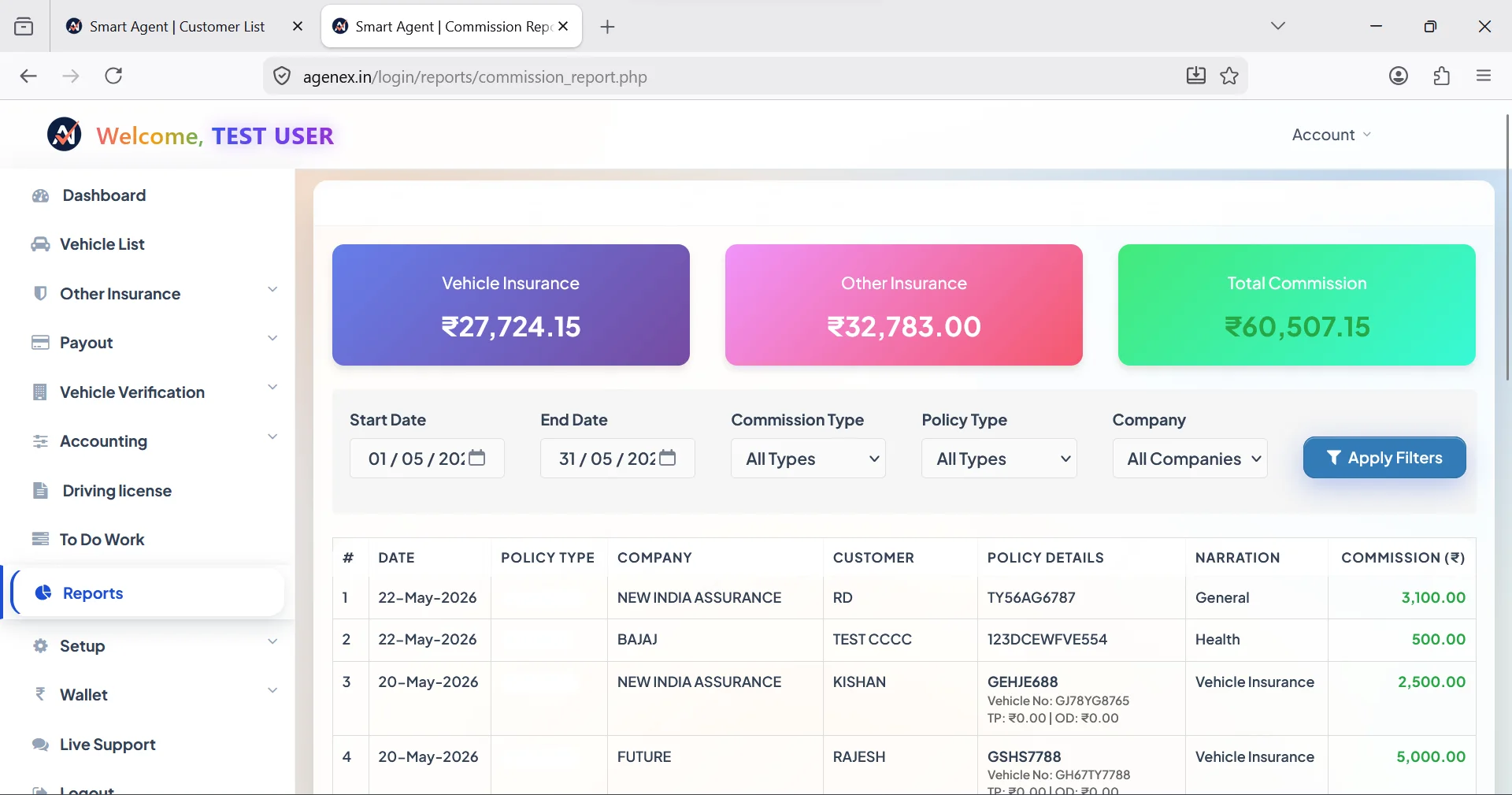

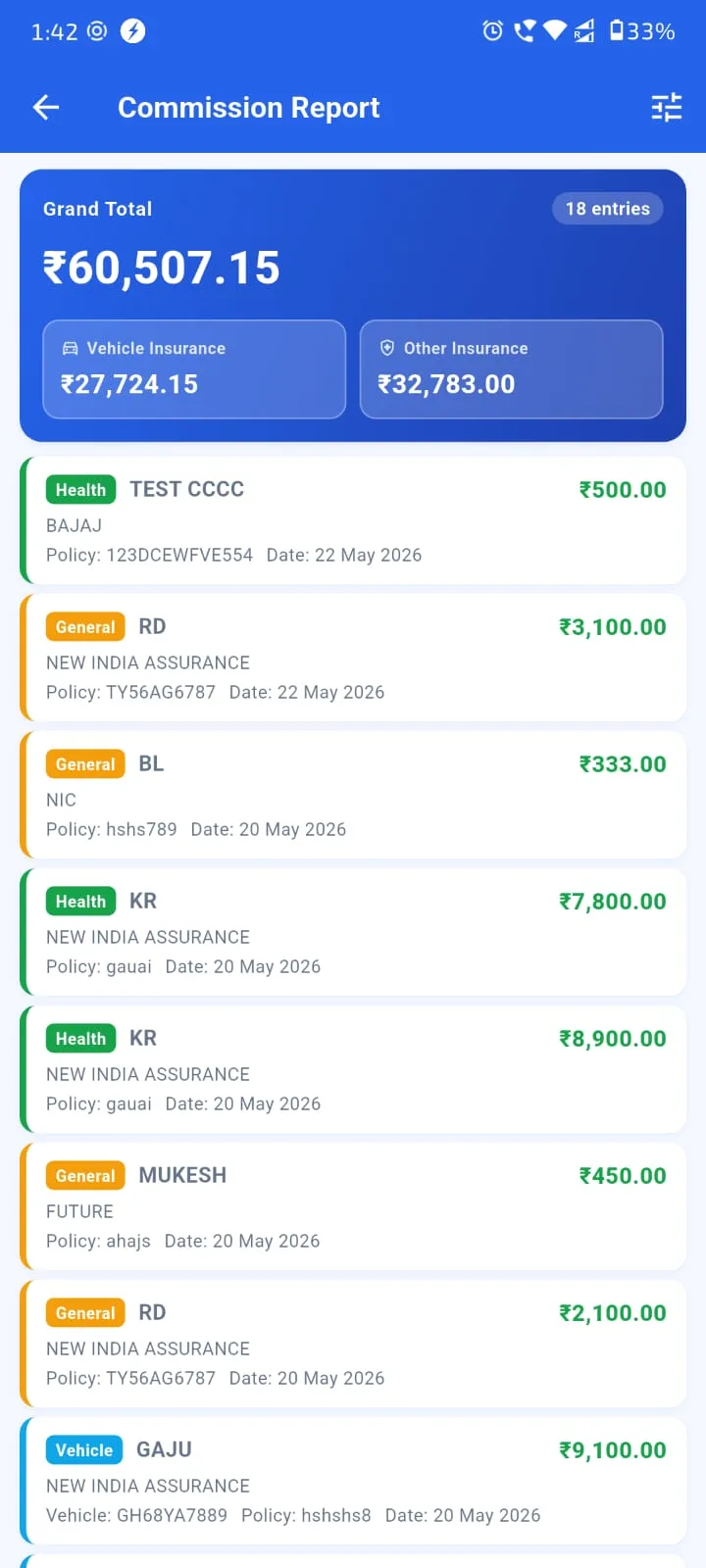

A working insurance agent app captures TDS on every commission entry, builds a per-insurer TDS summary throughout the year, and produces a year-end report that matches Form 26AS data from the income tax department. Year-end filing then becomes a 30-minute verification rather than a 3-day reconciliation. See Automated Commission Tracking.

Income Tax — How Commission Is Treated

For individual insurance agents, commission income is typically treated as either 'Income from Other Sources' or 'Business Income' (Profession), depending on whether you operate as a sole proprietor business or as an individual professional. The difference matters for which deductions you can claim.

Most active full-time agents file as 'Business Income' (Profession) — this allows broader expense deductions: mobile and internet bills, software subscriptions like your insurance digital assistant app, vehicle expenses for client visits, office rent, salary paid to staff or sub-agents, marketing expenses, training and conference fees, professional service fees (your CA), printing and stationery. Track these monthly in your insurance agency management software's accounting module rather than trying to reconstruct them at year-end.

Standard income tax slabs apply on net taxable income (gross commission - deductible expenses). Plan your tax-saving investments (Section 80C, 80D, 80CCD etc.) through the year, not just in March panic mode.

Try Agenex Free

Every Agenex feature is included on a free trial — no credit card required. The commission reconciliation software with year-round TDS and tax tracking.

Start Free TrialGST Applicability For Insurance Agents

GST treatment depends on your annual commission level. Below the GST registration threshold (currently Rs.20 lakhs in most states, Rs.10 lakhs in special category states), individual agents are exempt from GST registration. Above the threshold, GST registration becomes mandatory and you charge GST (typically 18%) on your commission services.

The practical implications: if you're a small solo agent with commission under Rs.20 lakhs annually, you don't need to worry about GST. If your network is growing and you're approaching the threshold, plan ahead — registration involves paperwork, monthly returns, and ongoing compliance. Some agencies cross threshold mid-year and have to register from that point onward.

For agencies operating with sub-agent networks, the GST conversation gets more complex — your gross commission may be high but the net (after sub-agent splits) is what you actually retain. A proper insurance agency management software with built-in GST handling helps you understand your exposure and prepare accordingly. Always confirm specifics with your CA — GST rules around insurance brokerage continue to evolve.

Year-End Filing Workflow

The cleaner your monthly records, the easier year-end filing becomes. A working workflow looks like:

- Monthly: Reconcile insurer commission statements against your in-system records. Track TDS deducted per insurer. Log business expenses in accounting module.

- Quarterly: Download Form 26AS, compare TDS reflected vs your records. Catch any insurer discrepancies early — easier to resolve in March than in October.

- Year-end (April-July): Generate annual commission summary from your insurance agent app. Share with CA along with expense ledger, TDS summary, sub-agent payout records (if applicable). CA files ITR — typically takes 1-2 weeks given clean data.

Agents who follow this rhythm consistently end up paying lower effective tax (because they claim every legitimate deduction), avoid scrutiny notices (because their records match 26AS), and spend almost zero stress at filing season. Insurance lead manage kaise kare ka equivalent for tax filing: build the discipline through the year, the year-end takes care of itself.

FAQ

Typically 5% under Section 194D (life) and 194H (general) when commission exceeds the prescribed threshold. Verify current rate with your CA — rates change with tax circulars.

Only if annual commission exceeds the GST registration threshold (typically Rs.20 lakhs in most states, Rs.10 lakhs in special category states). Below that, individual agents are GST-exempt.

Mobile + internet bills (business proportion), software subscriptions including your insurance agent app, vehicle expenses for client visits, office rent, staff salaries, sub-agent commission paid out, training, marketing, professional fees, printing and stationery. Maintain records — receipts and digital trails matter.

Download Form 26AS quarterly. Compare TDS entries against your in-system commission record per insurer. Discrepancies usually arise from insurer-side errors or timing — resolve them with the insurer in the same quarter rather than waiting for year-end.

Yes — the basic income tax exemption limit applies. Plus standard deductions and tax-saving investments under Section 80C, 80D etc. further reduce taxable income. Your CA optimizes this based on your full income picture.