Insurance agent income in India is one of the most variable in financial services. New agents in their first year often struggle with modest earnings. Established multi-line agents with mature books can earn substantially. The variability isn't random — it follows recognizable patterns based on book maturity, product mix, sub-agent leverage, and operational discipline. This guide explains how Indian insurance agent income actually compounds, why the renewal income matters more than first-year commission, and what the highest earners do differently. Verify all commission and tax rates with your CA and current insurer circulars — these change periodically. Related: Grow Insurance Agency India, Calculate Insurance Commission, GST & Income Tax Guide.

First-Year Commission — The Survival Phase

First-Year Commission (FYC) is the front-loaded commission you earn on a new policy. The percentages vary significantly by product line:

- Life insurance (LIC, term, endowment, ULIP): FYC typically 25-40% of first-year premium.

- Health insurance: FYC around 15-25% of premium.

- Motor insurance (Own Damage portion): Around 10-15% on OD premium; lower regulated commission on third-party.

- General insurance (Home, Shop, Fire): 10-15%, varies by insurer and product.

For most new agents in their first 12 months, income is volatile and modest. You're still building a customer base. Most months you sell a handful of policies. Income comes from FYC, with no meaningful renewal commission stream yet built up. This is the survival phase — getting through it requires either a financial cushion, a part-time approach (insurance as supplementary income while maintaining another job), or family support. Many new agents quit during this phase before the math turns favorable.

Why Renewal Income Matters More Than FYC

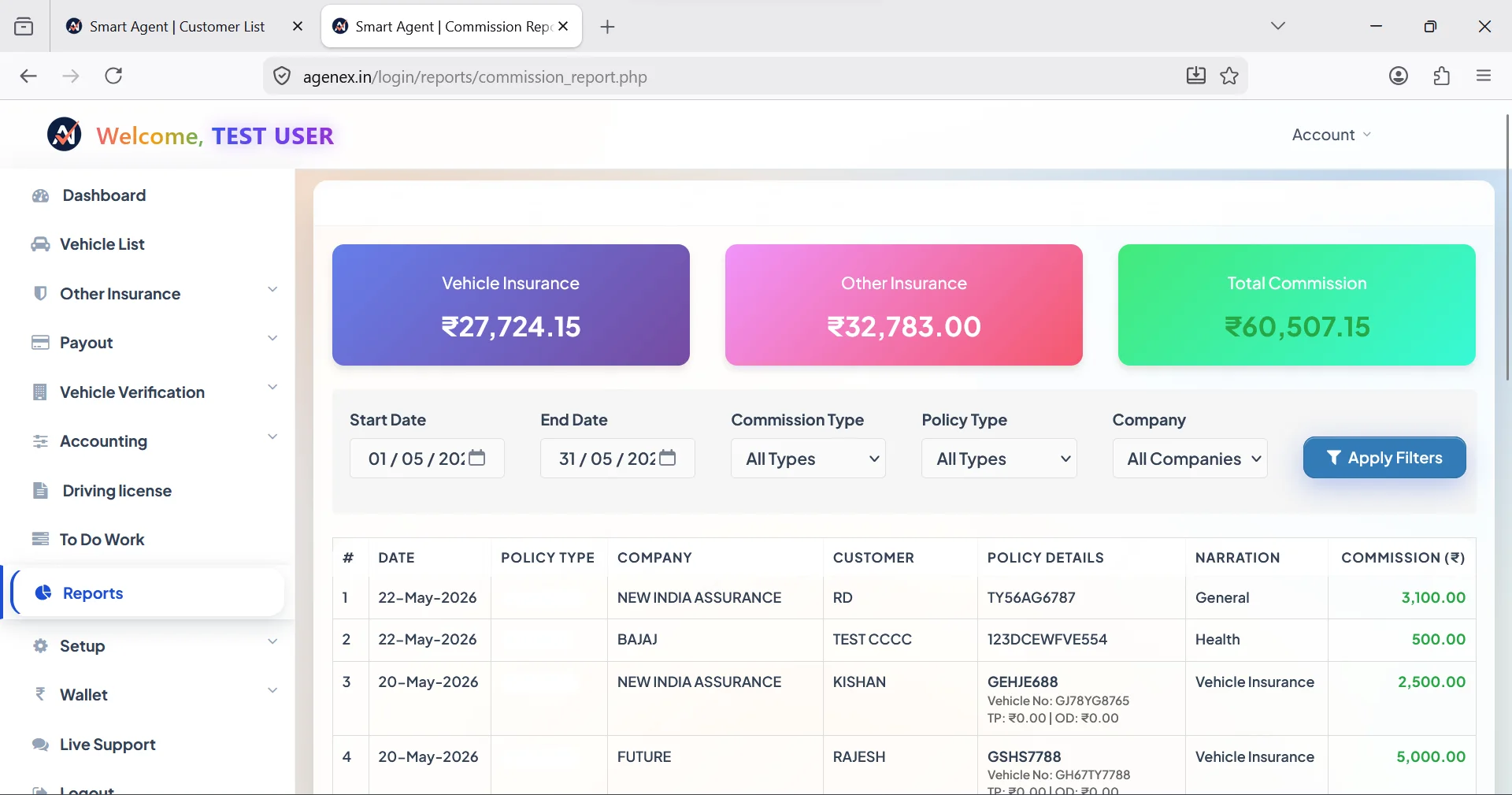

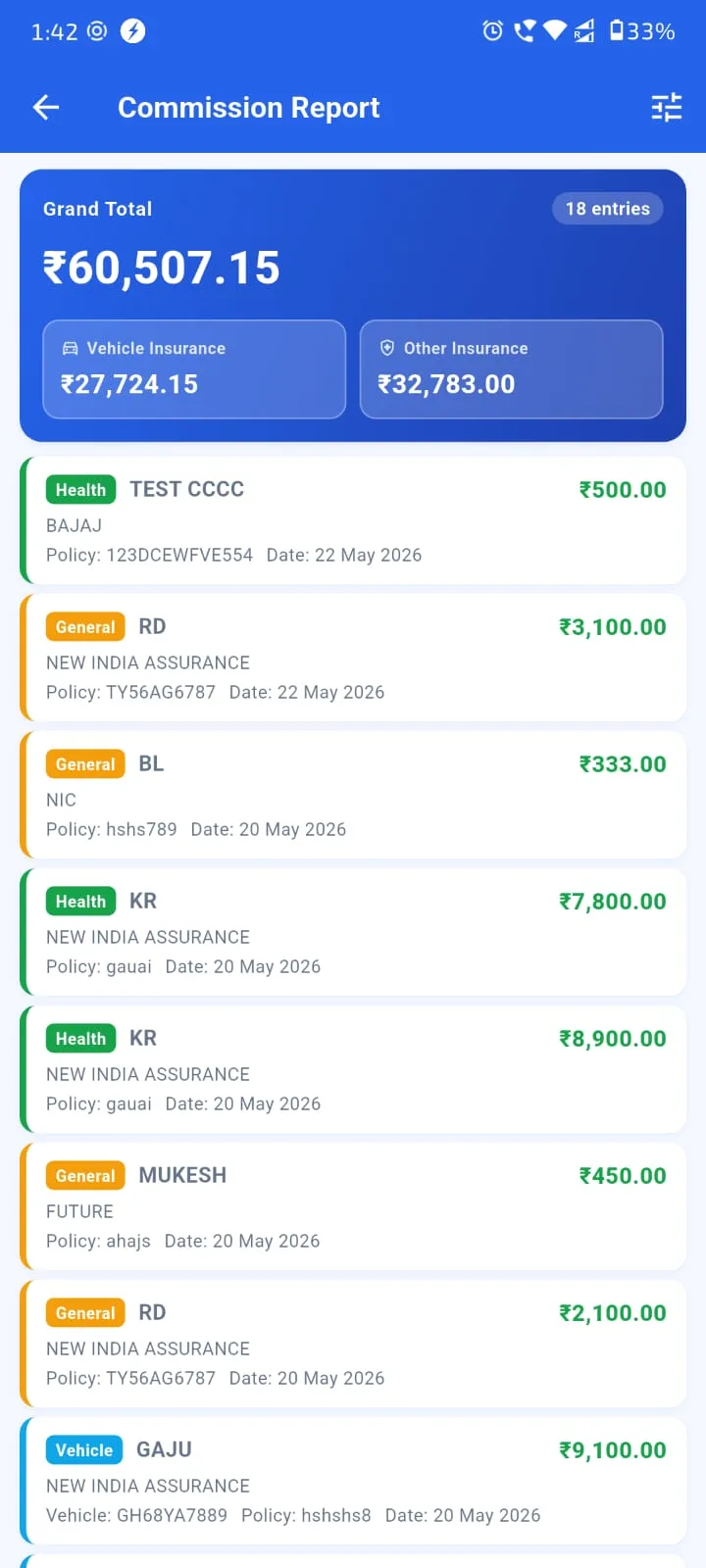

The crucial economic insight in insurance is this: FYC pays you for getting the customer; renewal commission pays you for keeping them. A 3-year-old book of 1,000 active policies, generating modest average renewal commission per policy, can deliver meaningful passive monthly income just from people renewing what they already bought.

This compounding is what makes insurance a wealth-building career rather than a transactional sales career. Year 1, you earn mostly FYC. Year 2-3, renewal commission starts becoming meaningful. By year 5+, renewal commission often equals or exceeds new business commission. By year 10, a well-maintained book generates substantial recurring income with manageable ongoing effort.

The critical condition: you must retain customers. A book that loses 30% of renewals annually never compounds. A book that retains 90%+ compounds beautifully. This is why a working customer renewal reminder software with proper 30/15/7/1 day WhatsApp cadence is the highest-ROI tool an agent can invest in. See Never Miss A Policy Renewal.

Try Agenex Free

Every Agenex feature is included on a free trial — no credit card required. The insurance agent app that protects renewal income for every agent.

Start Free TrialMulti-Line Strategy — The Income Multiplier

Single-line agents typically cap out at moderate income levels. The math: even with 800-1,000 customers, if you're selling only one product line (say, only motor insurance), your annual commission is constrained by the average premium and commission rate of that one line.

Multi-line agents — who serve the same customer across motor + health + life + general — multiply their commission per relationship significantly. The same customer who paid you motor commission also paid health commission, also paid life commission, also potentially pays travel or home insurance commission. Each line of business adds incremental income without needing a new customer.

This is why cross-sell discipline matters so much. A working insurance digital assistant app with cross-sell tagging (motor customers without health, health customers without term, etc.) systematically surfaces these opportunities. See Cross-Sell & Upsell AI. The best app for LIC agents specifically helps LIC-specialists add health and motor lines to their primarily-life book without losing their LIC focus.

Scaling Through Sub-Agents — The Mini-Agency Path

Solo agents have a time ceiling. There are only so many hours in a day to acquire customers, service renewals, handle claims, and manage operations. Around the 1,000-1,500 policy mark, most agents hit this ceiling — they can't grow further without either burning out or fundamentally changing their model.

The path forward is sub-agent / POSP network building. You onboard sub-agents under your code. Each sub-agent sells under your network. Commission auto-splits between sub-agent and you per the agreed slab. Your time becomes more managerial than transactional, but your income scales because multiple people are now selling under your structure.

This is the "mini-agency" stage — typically 3-5 active sub-agents, structured commission splits, formal monthly settlements. A working insurance agency management software with sub-agent module makes this manageable. See Sub-Agent Management System and POSP Agent Software. Insurance lead manage kaise kare at this stage becomes "manage the lead pipeline of multiple sub-agents simultaneously" — which only software can do at scale.

FAQ

Income in year 1 is highly variable. Many new agents earn modest amounts as they build their initial customer base. Strong first years are possible but uncommon; most successful careers ramp up over 2-3 years.

By year 3, renewal commission typically matches or exceeds new business commission for most agents who retained customers well. By year 5, renewal is usually the dominant income source.

Yes — many successful agents start part-time, using existing professional networks (family, neighbors, colleagues) for initial customer acquisition. Going full-time once the book reaches sustainable income is a common path.

Theoretically yes — there's no formal ceiling. Practically, individual agents top out at certain levels and growth beyond requires moving to sub-agent network or broker structure. Top earners in Indian insurance distribution operate at multi-agent or broker stage.

Yes — TDS is typically deducted at source by insurers when commission crosses the prescribed threshold. Verify current rates with your CA. See GST & Income Tax Guide.